As the Strait of Hormuz gradually reopens as of early April 2026, oil flows recover but risks shift toward the Strait of Bab al-Mandeb, where an Iranian proxy group threatens to disrupt shipping once again. In the previous analysis, structural risks associated with a prolonged disruption of the Strait of Hormuz were outlined. Recent developments indicate that, as anticipated, the situation is evolving toward a partial normalization. Traffic through the strait is gradually increasing, with a growing number of vessels transiting, most notably Pakistani and Iraqi exports. This effectively restores approximately 3 million barrels per day of crude flows through Hormuz. The drivers behind this reopening appear twofold. On one hand, a relative reduction in immediate escalation risk has lowered the incentive for full closure. On the other, the financial and operational burden of enforcing a sustained maritime blockade is likely constraining Iran’s ability to maintain comprehensive interdiction. The result is a phased reopening rather than a formal resolution.

Oil Markets: Partial Relief, Persistent Volatility

The return of Iraqi volumes provides tangible relief to global oil supply, but the market remains structurally tight. The reopening is incomplete, selective, and reversible. A significant portion of Gulf exports continues to face uncertainty, and shipping risk premiums remain elevated.

Moreover, the geopolitical backdrop remains fragile. The possibility of renewed escalation involving the United States continues to weigh on market sentiment. As a result, oil prices are expected to remain elevated and highly volatile in the coming weeks, with any sustained relaxation likely deferred toward June, contingent on further stabilization.

A Shifting Maritime Risk Landscape: Bab al-Mandeb

While Hormuz risk is gradually easing, a new threat vector is emerging further west. The potential entry of Ansarallah into the conflict introduces uncertainty around the Bab al-Mandeb Strait. Unlike Hormuz, Bab al-Mandeb is less critical for crude oil flows, but it is a vital artery for global cargo traffic, linking the Red Sea to the Suez Canal and onward to Europe.

Disruptions in this corridor would have a disproportionate impact on container shipping, bulk commodities, and supply chains, even if energy markets are less directly affected. This creates a shifting risk profile. While one chokepoint shows signs of reopening, another may become a source of instability, maintaining upward pressure on global freight costs and insurance premiums.

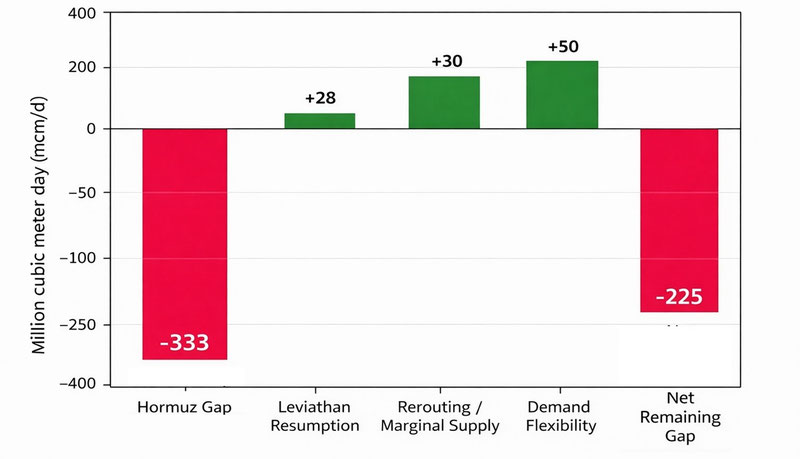

Natural Gas: Structural Deficit with Partial Relief

Natural gas markets continue to reflect a more severe and persistent disruption. The closure of Hormuz and the impact on Qatari gas infrastructure have resulted in a substantial LNG supply deficit. However, a broader view also includes disruption of Egyptian LNG exports, which rely on Israeli gas supply (also paused upon initiation of regional hostilities).

- Direct natural gas shortage from Hormuz disruption: ~305 mcm/day

- Broader natural gas shortage including regional impacts: ~333 mcm/day

The resumption of production at the Leviathan gas field in early April 2026 provides a measurable, though limited, offset. As the largest gas production site in Israel, Leviathan produces approximately 12 BCM/year (~33 mcm/day), of which most is directed to regional offtakers - CNG to Jordan for local use and supply to international markets via Egyptian-based LNG export terminals.

This reduces the global supply deficit by roughly 10%, bringing total shortages down from approximately 332.5 mcm/day to ~305 mcm/day. While this is a meaningful contribution at the regional level, it does not fundamentally alter the global balance. LNG markets remain tight, and pricing pressure is likely to persist until more substantial Gulf supply is restored.

Secondary Commodities: Emerging Supply Chain Effects

Beyond oil and gas, the disruption has had notable implications for other commodities tied to Persian Gulf exports:

- Sulfur, a byproduct of oil and gas processing, has experienced constrained availability due to reduced refining throughput in the region. Partial reopening of Hormuz should gradually ease supply, though logistics bottlenecks remain.

- Helium, for which Qatar is a major global supplier, continues to face export constraints. Even limited disruptions to Qatari facilities and shipping routes can significantly impact global availability due to the highly concentrated nature of supply.

These markets are particularly sensitive to logistics rather than production alone. As such, even incremental improvements in maritime access can have outsized effects on availability and pricing.

Cargo and Freight: Risk Redistribution

Global cargo flows are now caught between two evolving chokepoints. The easing of restrictions in Hormuz supports a gradual normalization of Gulf-origin trade. However, the potential destabilization of Bab al-Mandeb introduces new uncertainty into East-West shipping routes.

This dynamic is likely to result in continued elevated freight rates, increased insurance and rerouting costs, greater volatility in delivery times and supply chains. In effect, risk is not disappearing, but rather shifting geographically.

tight and volatile

The gradual reopening of the Strait of Hormuz confirms earlier expectations that a complete and sustained blockade would be difficult for the Islamic Republic of Iran to maintain. The reported return of Iraqi oil flows in early April 2026 provides relief to global oil markets, but does not eliminate the underlying fragility. Oil markets remain tight and volatile, with meaningful stabilization likely only toward June 2026, if current trends continue. Natural gas markets continue to face a significant structural deficit, only partially offset by regional production recovery such as the Leviathan field.

At the same time, emerging risks around the Bab al-Mandeb Strait highlight the evolving nature of maritime chokepoint vulnerability. The global energy and trade system remains exposed, not to a single point of failure, but to a network of interdependent risks. In this environment, volatility is not a temporary anomaly, but a structural feature of the current geopolitical landscape.

Interested in getting more global energy insights? You are welcome to contact Leon @LNRGTech.

Write a comment