The near-total disruption of the Strait of Hormuz oil transit route is now in its third week as of mid-March 2026, as the escalating U.S.-Israeli conflict with Iran is creating perhaps the most severe supply shock in modern oil market history. This analysis evaluates its operational and strategic consequences, focusing on quantitative pipeline bypass capacities, potential responses from alternative non-Gulf supply sources, and the resulting market dynamics including price trajectories and inventory pressures. Data are drawn from established infrastructure metrics and production outlooks as of early 2026 to assess whether rerouting and incremental non-Gulf production can mitigate the shortfall, without reliance on speculative assumptions. The Strait of Hormuz accounted for an average of approximately 20 million barrels per day (mb/d) of crude oil and petroleum products in 2025, representing roughly 20% of global seaborne oil trade. Of this volume, crude and condensate flows totaled around 15–16 mb/d, with key origins including Saudi Arabia (approximately 5.5 mb/d), Iraq, the UAE, Kuwait, and Iran itself. In the current scenario, tanker loadings have slowed to a trickle, prompting Gulf producers to curtail output and fill onshore storage, resulting in an effective regional supply reduction estimated at 8–10 mb/d in the initial phase of disruption.

Mideast Bypass Pipeline Capacity and Partial Mitigation Potential

Two primary inter-state midstream assets provide direct alternatives to Hormuz routing for Gulf crude:

- Saudi Arabia’s East-West Pipeline (Petroline), running 750 miles from Abqaiq-area fields to the Yanbu terminal on the Red Sea. Design capacity has been expanded to 5–7 mb/d following recent upgrades, with Aramco confirming ramp-up toward sustained full utilisation. Export loading constraints at Yanbu limit net incremental export potential to approximately 4.5–5 mb/d under current configuration, though operational flexibility allows redirection of volumes previously destined for Hormuz.

- The UAE’s Abu Dhabi Crude Oil Pipeline (ADCOP/Habshan-Fujairah), spanning 248 miles from onshore Habshan fields to the Fujairah terminal on the Gulf of Oman. Nameplate capacity stands at 1.5–1.8 mb/d, with current utilisation leaving modest spare headroom (estimated 0.4–0.7 mb/d incremental) before maximum throughput.

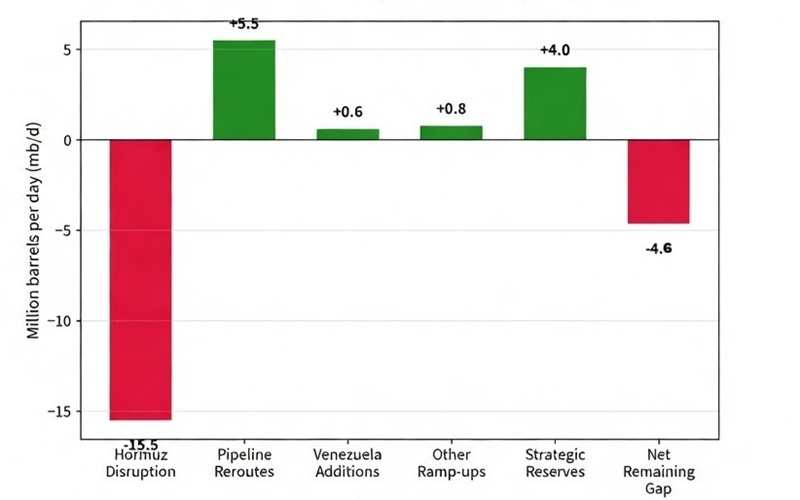

Combined, these bypass pipeline routes offer an effective rerouting capacity of approximately 4–7 mb/d once fully mobilised, depending on maintenance

schedules and terminal loading rates. This represents 20–35% of pre-disruption Hormuz crude flows but falls well short of offsetting the full volume

affected, particularly for producers lacking parallel infrastructure (Iraq’s southern fields, Kuwait, and Qatar remain fully exposed, with no comparable bypass options operational). Historical

precedents, including temporary Red Sea routing shifts in 2024, confirm that such pipelines can sustain partial flows without immediate technical failure; however, sustained operation at peak

rates introduces logistical constraints on storage, blending, and tanker availability at alternative terminals. Iraq’s Kirkuk–Ceyhan line offers negligible relief due to prior security-related

outages and limited capacity.

In theory, it is also possible to reroute at least some of the liquids via trucks, or so called "road tankers", but the capacity would be negligible. In aggregate, existing Mideast bypass

infrastructure can therefore absorb only a fraction of the shortage in the initial 3-month window, leaving a structural gap of 10–15 mb/d that must be

addressed through inventory drawdowns or non-Gulf incremental supply. This is also pending that Iran is not able to cause damage to the above mentioned pipelines and affiliated ports in the Saudi

Arabia and UAE,

Venezuela Regime-Change Impact: Reopening of Paused Wells and Stockpile Release

Following the political transition in Venezuela earlier in 2026, the country’s upstream sector-possessing the world’s largest proven reserves at over 300 billion barrels - presents a measurable but time-bound source of additional barrels. Current output stands near 0.8 mb/d, constrained by decades of underinvestment and sanctions-era infrastructure degradation. Regime change enables immediate reopening of paused wells and well interventions, with industry estimates indicating a feasible short-term uplift of 0.1–0.4 mb/d within the first three months under sanctions relief and renewed access for international operators. This ramp reflects targeted workovers in mature fields and utilisation of existing upgraders (e.g., Petropiar). Beyond production gains, gradual drawdown of available commercial and strategic stockpiles. interpreted here as an aggregate 40–50 million barrels releasable over approximately four months, equates to an average incremental flow of roughly 0.33–0.42 mb/d during the initial period, assuming orderly export logistics.

Combined, Venezuelan reopening and stockpile release can therefore contribute 0.43–0.82 mb/d of additional supply in the near term, providing a meaningful but partial offset to the Hormuz gap. Longer-term recovery toward 1.2–1.5 mb/d by end of 2026, or potentially 2.0–2.5 mb/d over a decade with sustained investment, lies outside the short-term 3-month assessment horizon.

Incremental Production Capacity from Non-Aligned Producers

With Russia maintaining restrained output under existing OPEC+ frameworks and members such as Algeria adhering to aligned policy positions, attention shifts to spare or flexible capacity elsewhere. Saudi Arabia and the UAE are excluded from this tally to avoid double-counting their bypass pipeline contributions.

Non-OPEC+ producers dominate near-term flexibility:

- The United States (shale basins) retains operational headroom for modest acceleration via completions and drilling optimisation, though rapid response is tempered by supply-chain and labour constraints; incremental potential in the 3-month window is estimated at 0.20–0.50 mb/d under current market incentives.

- Guyana and Brazil continue steady ramp-ups from new deepwater projects, adding collectively 0.30–0.50 mb/d annually, with a portion (approximately 0.15–0.25 mb/d) realisable in the near term through optimised field scheduling.

- Canada offers limited additional barrels from oil-sands and conventional adjustments (circa 0.10–0.20 mb/d feasible short-term).

- Other non-OPEC streams (e.g., Norway, Mexico) provide marginal upside but no significant spare beyond baseline growth forecasts.

Aggregate incremental production from these sources is conservatively assessed at 0.5–1.0 mb/d over the next three months, constrained by project timelines and the absence of large-scale spare capacity outside OPEC+ core members. No material contributions are anticipated from Iran-aligned or Russia-constrained entities within the specified exclusions.

Net Shortage Assessment and Oil Price Implications Over the Next Three Months

Summing the above:Hormuz net disruption of approximately 15–18 mb/d (after accounting for Iran’s own curtailed exports) is partially mitigated via bypass pipelines: 4–7 mb/d, Venezuela contribution: 0.4–0.8 mb/d and other eligible incremental production: 0.5–1.0 mb/d. This yields a remaining structural shortage of roughly 7–12 mb/d in the near term, partially buffered by global inventory drawdowns (including emergency releases). Over a sustained three-month period, the cumulative shortfall equates to 630–1,080 million barrels, assuming no swift resolution of the Hormuz routing.

Oil prices have already risen from $73/bbl in late February to $103/bbl by mid-March in response to the initial disruption. With bypass and alternative supply covering less than half the gap, and global spare capacity outside the excluded producers remaining tight, the market faces continued upward pressure. Historical correlations between chokepoint disruptions and price responses suggest that a net shortage of this magnitude, unmitigated by full OPEC+ flexibility, will support Brent crude in the $110–130/bbl range over the ensuing three months, subject to duration of the conflict, inventory release efficacy, and demand elasticity. Should rerouting stabilise at higher utilisation rates or Venezuelan flows exceed lower-bound estimates, the upper end of this band may moderate; conversely, prolonged closure without additional offsets would sustain or elevate levels beyond current observations.

The data indicate that while Mideast bypass infrastructure and select non-Gulf responses provide partial resilience, they fall short of fully neutralising the Hormuz shortfall in the near term. Long-term pipeline and upstream investments could enhance future stability, yet the immediate outlook underscores the enduring importance of diversified midstream routes and flexible non-OPEC supply chains for regional and global energy security.

Interested in getting more global energy insights? You are welcome to contact Leon @LNRGTech.

Write a comment