The rapid expansion of Lithium ion (Li-ion) battery production worldwide and parallel driven expansion of lithium mining continues. This survey brings the updated 2022 analysis of raw Lithium production worldwide, providing supply and demand projections for the mid and long-term. The study implies that Li-ion is due to retain its role as the dominant technology for electric energy storage through this decade, but critical outlook on global Lithium resources in terms of supply and demand is important in order to prepare for potential disruptions in this market. Shifts in production and consumption may also contain hints to upcoming Lithium-ion utilization trends and the competitiveness of alternative battery technologies.

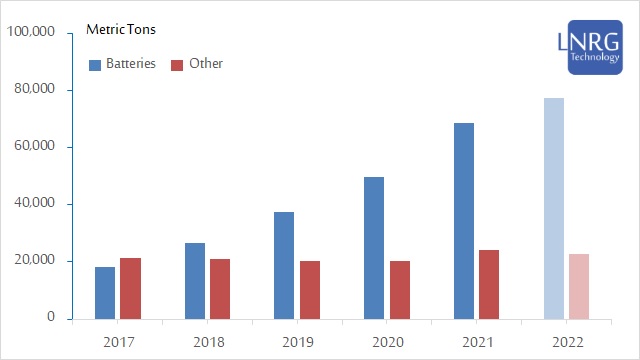

Lithium is a metal, which can be found in the form of Lithium salts in various locations across the globe and when found in sufficient concentrations – such locations are identified as Lithium resources. Currently, Lithium resources are utilized by a number of end-use industries, including manufacturers of Lithium-based batteries, ceramics & glass, greases, air treatment devices, casting mold powders, polymers and more. Since 2018, the most dominant utilization of Lithium has recently become electrochemical Li-ion cells and with current rapid expansion of battery production, it is assumed that batteries would be an overwhelmingly dominant target market for Lithium resources for at least a couple of decades.

There are several variants of Li-ion battery technology on the market, the most common being Lithium Iron Phosphate (LFP), Lithium Nickel Manganese Cobalt (Li-NMC or simply NMC) and Lithium Nickel Cobalt Aluminum Oxide (Li-NCA or simply NCA). Less common technology is the somewhat outdated Lithium Cobalt Oxide (LCO) cathode electrode with Lithium salts as electrolyte and carbon as an anode, which altogether require a considerably larger amount of Lithium and Cadmium metals per cell. Other niche Li-ion technologies are Lithium Manganese Oxide (LMO) and Lithium Titanate (LTO), which are not principally different, with some variance of Lithium-containing cathodes and electrolytes coupled with a number of anode types achieving slightly differing power, cycle and specific density figures. It can also be mentioned that Solid State Lithium and Lithium Sulfur (Li-S) are potentially nearing the commercialization horizon. The growth of the Li-ion battery industry would obviously require a parallel expansion of Lithium mining and processing enterprises – mainly targeted on producing high-grade Lithium carbonate and to a lesser degree on Lithium chlorate and Lithium hydroxide.

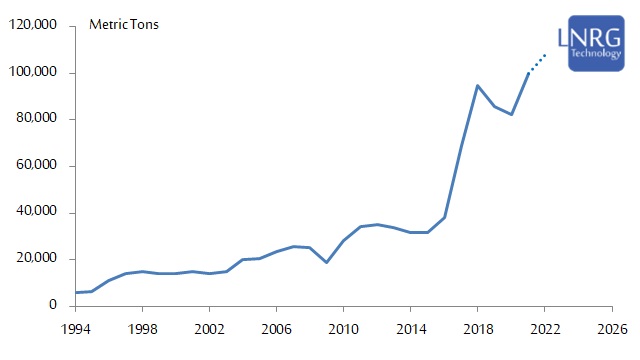

According to the US Geological Survey (USGS), the global production of Lithium reached a whopping 100,000 tons annually in 2021. This should be added with the unreported US production, which is likely somewhere around 870 metric tons annually. The global Lithium production capacity well surpassed 100,000 tons, adding significant expansion of Lithium mining businesses worldwide, led by Australia and South America. The global 2021 demand for Lithium was estimated at 93,000 metric tons, presenting a strong annual growth over previous year – mostly due to rapid expansion of Li-ion battery production facilities for electric vehicles. LNRG Technology estimates that the Lithium production capacity is set to expand in 2022 to over 107,000 metric tons, but still lagging beyond Lithium demand surge in the batteries industry which would alone require some 80,000 metric tons this year. A much greater production capacity expansion is expected in 2023-25, catching up to the demand and likely easing the supply strain.

Li-ion batteries are the unquestionable rulers of energy storage devices in portable electronics and the emerging electric mobility and grid storage. With the developing demand of battery manufacturers, Lithium production and processing industries are undergoing a rapid expansion. Despite the ramp-up of Li-ion battery production worldwide and parallel expansion of lithium mining, there are several questions posed for the mid and long-term prospects of this industry. While, in the mid-term there are potential technological drivers, capable to raise competition to the Li-ion technology, on the longer term there are also potential constaints in Lithium supply. There are also more acute challenges in acquisition of rare elements such as Cobalt, but some Li-ion chemistries do not require it and hence it is not the focus of this research.

One of the questions posed in this study is for how long Lithium mining and production expansion is set to go on before reaching its peak, as Lithium resources in Earth's crust are limited. The latest USGS estimate for available Lithium reserves and resources in early 2022 was at 22.0 million and 89.0 million metric tons respectively. Theoretically, with current production rates, known Lithium reserves would be sufficient to sustain production for over 200 years, while resources can prove sufficient for almost a thousand years. This is however an over-simplification, disregarding the rapid production growth and dynamic market constraints.

Another question to ask is whether it is possible to have a more realistic estimate for future rates of Lithium production. This can be achieved by a combination of predictive analytics and a fundamental assessment of resources. First of all, the known reserves and resources of Lithium are periodically supplemented with new discoveries. During the past two decades known Lithium resources have increased several fold and there is a reason to believe this is not the end of Lithium resource discoveries. Nevertheless, Lithium is still an uncommon element in Earth's crust and thus there is a slim chance for further multiple fold growth from current estimates, unless new technologies for Lithium production from low-concentrated brines are brought to the market.

Please contact us for more details on the Lithium market. The extended commercial report can be purchased at LNRG Technology digital store (below).